The Federal Housing Administration (FHA) is a United States government company founded by President Franklin Delano Roosevelt, created in part by the National Housing Act of 1934. The FHA insures home mortgages made by personal loan providers for single household properties, multifamily rental residential or commercial properties, health centers, and residential care facilities. FHA home loan insurance coverage safeguards lenders against losses.

Since loan providers handle less threat, they are able to offer more home mortgages. The objective of the company is to assist in access to budget friendly home loan credit for low- and moderate-income and novice homebuyers, for the building and construction of cost effective and market rate rental homes, and for medical facilities and residential care facilities in communities throughout the United States and its territories.

Wade was verified by the U.S. Senate on July 28, 2020 as the FHA Commissioner. It is different from the Federal Housing Financing Agency (FHFA), which supervises government-sponsored enterprises. Throughout the Great Anxiety lots of banks failed, triggering a extreme decline in home mortgage and ownership. At that time, the majority of home mortgages were short-term (3 to five years), without any amortization, and balloon instruments at loan-to-value (LTV) ratios listed below sixty percent.

Not known Facts About What Is The Percentage Of People Who Pay Off Mortgages

The banking crisis of the 1930s required all lending institutions to retrieve due home loans; refinancing was not available, and numerous debtors, now jobless, were unable to make home loan payments. As a result, lots of houses were foreclosed, causing the housing market to plunge. Banks gathered the loan collateral (foreclosed houses) however the low home worths resulted in a relative lack of possessions.

The National Real Estate Act of 1934 developed the Federal Real estate Administration. Its objective was to manage the interest rate and the regards to mortgages that it insured; however, the brand-new practices were restricted only to white Americans. These brand-new lending practices increased the variety of white Americans who might afford a down payment on a house and monthly debt service payments on a home loan, therefore likewise increasing the size of the market for single-family houses.

The 2 essential were "Relative Economic Stability", which constituted 40% of appraisal worth, and "protection from unfavorable impacts", which made up another 20%. In 1935, the FHA provided its appraisers with an Underwriting Manual, which provided the following guideline: "If an area is to retain stability it is essential that residential or commercial properties shall continue to be inhabited by the exact same social and racial classes.

The Single Strategy To Use For After My Second Mortgages 6 Month Grace Period Then What

Due to the fact that the FHA's appraisal requirements included a whites-only requirement, racial segregation ended up being a main requirement of the federal home mortgage insurance coverage program, as the FHA frequently timeshare presentation deals 2016 judged any homes in racially blended areas or in close distance to black neighborhoods as being high-risk. While this practice is no longer main policy, its practices are still widely carried out in procedures of de facto partition. [] In 1935, Colonial Town in Arlington, Virginia, was the very first massive, rental housing task put up in the United States that was Federal Housing Administration-insured (how did clinton allow blacks to get mortgages easier).

In 1965 the Federal Real estate Administration entered into the Department of Real Estate and Urban Development (HUD). Following the subprime mortgage crisis, FHA, together with Fannie Mae and Freddie Mac, ended up being a big source of home mortgage funding in the United States. The share of home purchases funded with FHA mortgages went from 2 percent to over one-third of mortgages in the United States, as standard mortgage financing dried up in the credit crunch.

Joshua Zumbrun and Maurna Desmond of have composed that eventual federal government losses from the FHA could reach $100 billion. The troubled loans are now weighing on the firm's capital reserve fund, which by early 2012 had fallen listed below its congressionally mandated minimum of 2%, in contrast to more than 6% two years earlier.

Getting The What States Do I Need To Be Licensed In To Sell Mortgages To Work

Since 1934, the FHA and HUD have actually insured nearly 50 million house mortgages. Currently, the FHA has around 8. 5 million insured single household home mortgage, more than 11,000 insured multifamily home loans, and over 3,900 home loans for hospitals and residential care facilities in its portfolio. Home mortgage insurance coverage secures lenders from the effects of a home mortgage default.

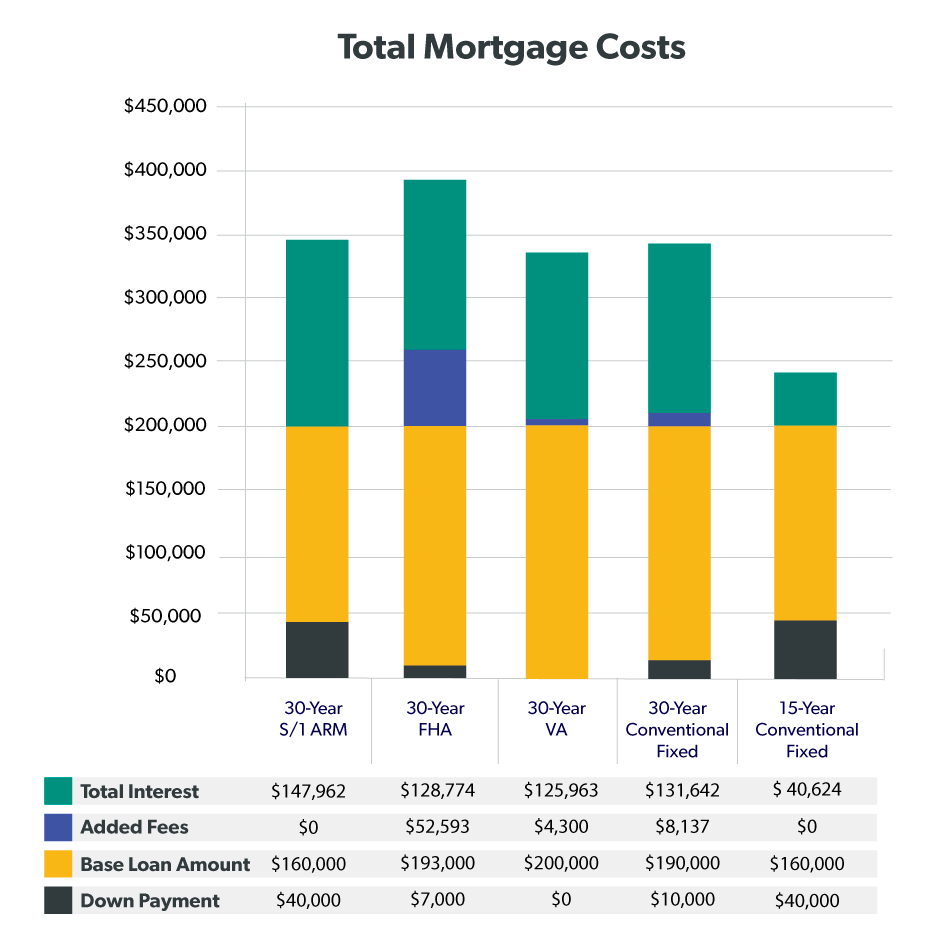

If the lending institution is FHA authorized and the mortgage fulfills FHA requirements, the FHA provides home mortgage insurance that may be more affordable, specifically for higher-risk customers Lenders can normally acquire FHA mortgage insurance coverage for 96. 5% of the assessed value of the home or building. FHA loans are guaranteed through a combination of an in advance home loan insurance coverage premium (UFMIP) and yearly home loan insurance premiums.

25% of loan worth (depending upon LTV and period), paid by the debtor either in money at closing or funded through the loan. Annual mortgage insurance premiums are consisted of in regular monthly home loan payments and range from 0 1. 35% of loan value (again, depending upon LTV and period). If a customer has bad to moderate credit rating, FHA home loan insurance might be less pricey with an FHA insured loan than with a traditional loan no matter LTV sometimes as little as one-ninth as much depending on the customer's credit history, LTV, loan size, and approval status.

Our How Does The Trump Tax Plan Affect Housing Mortgages Statements

Standard home loan premiums surge considerably if the customer's credit rating is lower than 620. Due to a sharply increased danger, most home mortgage insurance providers will not compose policies if the borrower's credit history is less than 575. When insurers do compose policies for borrowers with lower credit rating, annual premiums might be as high as 5% of the loan amount.

The 3. 5% requirement can be pleased with the customer using their own money or getting an eligible gift from a household member or other qualified source. The FHA insurance payments consist of 2 parts: the in advance home loan insurance coverage premium (UFMIP) and the annual premium remitted on a month-to-month basisthe shared mortgage insurance (MMI).

It includes a certain quantity to your month-to-month payments. Unlike other forms of standard funded home mortgage insurance, the UFMIP on an FHA loan is prorated over a three-year duration, significance should the homeowner refinance or offer throughout the first three years of the loan, they are entitled to a partial refund of the UFMIP paid at loan inception - what kind of mortgages do i need to buy rental timeshare reviews properties?.

The What Does It Mean When People Say They Have Muliple Mortgages On A House Ideas

The insurance coverage premiums on a 30-year FHA loan which began before 6/3/2013 must have been paid for at least 5 years. The MMI Find more information premium gets terminated immediately as soon as the unsettled principal balance, leaving out the in advance premium, reaches 78% of the lower of the preliminary prices or evaluated value. After 6/3/2013 for both 30 and 15-year loan term, the monthly insurance coverage premium must be spent for 11 years if the initial loan to worth was 90% or less.

A 15-year FHA mortgage yearly insurance premium will be cancelled at 78% loan-to-value ratio regardless of the length of time the premiums have actually been paid. The FHA's 78% is based upon the initial amortization schedule, and does not take any extra payments or brand-new appraisals into account. For loans begun after 6/3/2013, the 15-year FHA insurance premium follows the very same guidelines as 30-year term (see above.) This is the big difference between PMI and FHA insurance coverage: the termination of FHA premiums can barely be sped up.

PMI termination, nevertheless, can be accelerated through additional payments. For the 78% rule the FHA utilizes the original worth or purchase rate, whichever is lower, they will not go off a brand-new appraisal even if the value has actually increased. The creation of the Federal Real estate Administration successfully increased the size of the housing market.